Deploy Friday: Twelfth Edition

Mega IPOs, model lockdowns, and a seed market that forgot how to write cheques.

The week’s news keeps circling the same uncomfortable truth: the AU/NZ ecosystem is extraordinarily good at producing capital, and increasingly bad at getting it to the people who need it earliest. Techstars is gone, Callaghan is on the chopping block, seed funding fell 51% last year, and yet… Phonely just closed a A$22M Series A, Syenta raised A$37M for chip packaging. Meanwhile, Anthropic dropped a model capable of cracking bank security and immediately locked it away from most of the world, SpaceX filed the largest IPO in history, and Canva decided the public markets can wait. — Júlia G.

Top News

Anthropic’s Most Consequential AI Release in History

Anthropic released Mythos, an AI model capable of finding and exploiting vulnerabilities in the software running banks, power grids, and governments… then locked it down to 11 US-based partners. The Bank of England warned it could “crack the whole cyber-risk world open.” The EU, China, and Russia weren’t invited.

SpaceX Files for the Largest IPO in History

SpaceX has filed confidentially for a US$2 trillion IPO targeting US$75 billion in proceeds, which would still represent just 3.75% of the company. To accommodate it, Nasdaq scrapped its 10% minimum free float requirement and cut the seasoning period. That means $600 billion in passive NASDAQ 100 funds automatically buys in the moment it lists.

Canva Delays IPO to 2027 and Launches AI 2.0

Canva won’t be listing this year. COO Cliff Obrecht says the company wants its AI business model “bedded in” before facing public market scrutiny. While they wait, Canva launched AI 2.0 (conversational design, agentic orchestration, memory library) and kept the M&A machine running: Simtheory, Ortto, Doohly, Mango.AI, and Cavalry all acquired in 2026 alone.

The Accelerator Vacuum: Who’s Filling the Gap Left by Techstars?

In early 2026, NSW’s startup ecosystem lost its most generous first-cheque writer. Techstars Sydney, after three cohorts and 36 startups, shut its doors following the NSW government denial to renew its contract. The government pointed to its new $4 million diversity pre-accelerator as an alternative; a cold comfort for the 560 founders who had applications queued for Techstars. This, however, wasn’t an isolated decision. SXSW Sydney was defunded the same month. The Sydney Startup Hub shuttered before that. MVP funding was cut. The deeper story is structural, and the consequences are only beginning to show.

The Techstars model was never designed to survive on local terms. The original pitch, a world-class global brand validates AU/NZ founders, runs on government subsidy for three years, then sustains itself, had an expiry date baked in from day one. What it never solved was governance. Over time, Techstars centralised around corporate innovation partnerships and fee capture at its Boulder headquarters. It’s a pattern that’s played out elsewhere: Techstars has quietly retreated from Seattle and Austin too, markets far larger than Sydney. The same structural fragility is now visible across the Tasman, where the New Zealand government has moved to dissolve Callaghan Innovation, the crown entity underpinning much of the country’s early-stage tech infrastructure, leaving multiple accelerator programs contingent on a funding review that hasn’t concluded. Two governments, two ecosystems, one lesson: infrastructure that depends on a budget cycle is infrastructure with a countdown timer.

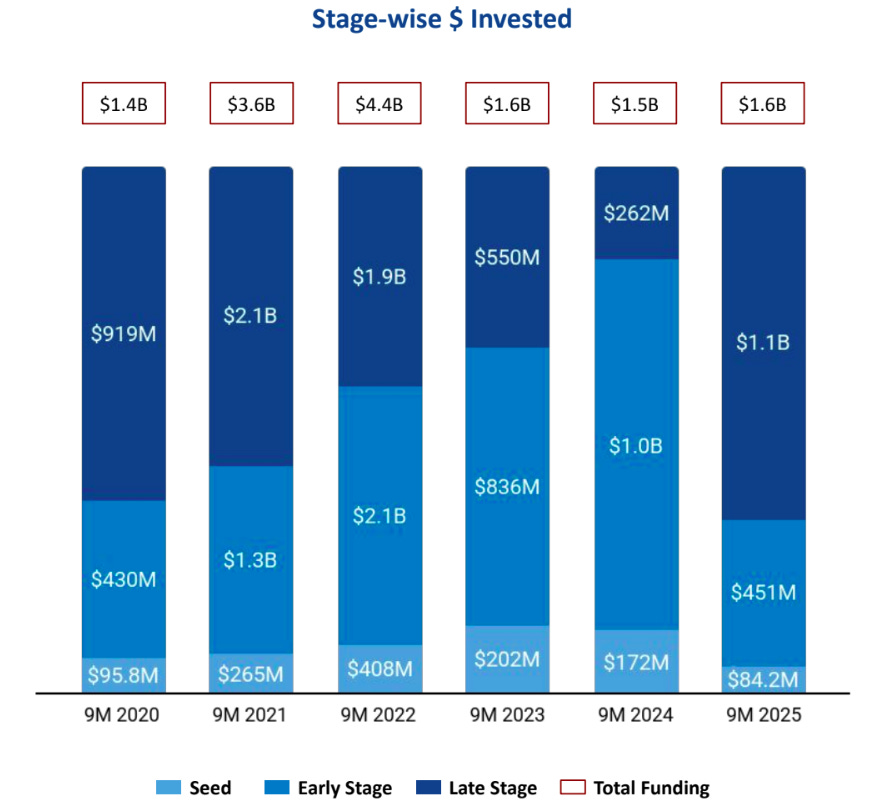

The consequences of that countdown are already visible in the funding data. Australia raised A$5.4 billion across 390 deals in 2025, the third-largest funding year on record. The ecosystem produces 1.22 unicorns per billion dollars invested. But strip back the top-line and the picture changes fast: the top 20 rounds captured 58% of all capital, seed funding fell 51% to $84 million, and early-stage rounds dropped 56% to $451 million… while late-stage capital surged 318%. The ecosystem is producing capital at record levels and directing almost none of it toward the stage where accelerators actually operate.

What remains is being asked to do more with the same resources. Startmate’s Summer ‘26 cohort, with 19 companies, 42 founders, and A$2.28 million deployed, was framed by new CEO Phoebe Pincus as proof that ANZ can produce globally competitive technology companies. Antler’s next Australian residency, its 16th, opens in July 2026 across Sydney, Melbourne, and Brisbane, continuing its Day Zero model of helping founders form teams and validate ideas before a product exists. Both programs are doing serious work, but neither was designed to absorb the volume that Techstars handled. In New Zealand, Icehouse Ventures targeted NZ$30 million for Seed Fund IV and closed at a record NZ$70 million from 363 investors, most of them local; a signal that private conviction is moving faster than public policy. But Startmate, Antler, and Icehouse together back fewer than 50 AU/NZ companies per cycle.

The deeper question isn’t whether the accelerator model is broken, but whether the region has a coherent answer for what comes next. University programs like UNSW Founders are absorbing the deep tech and hardware founders that cohort programs were never equipped to serve. Operator-led angel networks built by Canva, Atlassian, and Culture Amp alumni are recycling capital informally, without infrastructure, without overhead. Venture studios are gaining ground as an alternative for founders who need execution support rather than a curriculum: a structure where the idea gets validated and the product gets built before a founder even takes the reins. All of them are partial answers to a structural problem that neither the NSW nor the New Zealand government has shown much appetite to solve. The AU/NZ startup ecosystem is efficient, resilient, and increasingly self-reliant. It also just lost one of the mechanisms specifically designed to let someone in from the outside, and nobody has announced what replaces it.

🔥 Big Builds

→ Major launches, raises, or breakthroughs.

Phonely, the San Francisco-based (Melbourne-spun-out) AI call receptionist platform, raised A$22 million Series A to scale its AI receptionist across thousands of businesses.

Syenta, the Sydney-based ANU spinout developing lithography-free chip packaging technology, raised A$37 million Series A to commercialise its LEM process for AI data centres and expand into Arizona.

Ideally, the Auckland-based AI-powered consumer insights platform used by Google, Telstra and DoorDash, raised NZ$10 million Series A to accelerate US expansion.

Atomic Tessellator, the Auckland-based deep tech startup using quantum physics and AI to design rare earth alternatives, raised A$11.3 million seed to build an in-house lab and scale materials production for defence, semiconductor, and aerospace applications.

Renewable Metals, the Perth-based lithium-ion battery recycling startup, raised A$12 million Series A to bring its Kewdale demonstration plant online and develop a second commercial facility in the Hunter region.

Caruso, the Auckland-born AI fund administration platform managing $80B+ across 900 funds, raised A$9.3 million Series A to expand AI agent capabilities and grow headcount across Sydney, Auckland, and Dallas.

Clean Slate Clinic, the Sydney-based virtual alcohol detox social enterprise, raised A$4.3 million (including a A$2.8M convertible note) ahead of a A$10 million Series A targeting UK expansion in 2027.

Deteqt, the Sydney-based University of Sydney spinout building diamond quantum chips for magnetic sensing, raised A$5 million seed to develop field-ready quantum magnetometers for defence, mining, and medical applications.

Uluu, the Perth-based seaweed-derived plastic alternative startup, secured A$2.1 million from the Australian Government’s Industry Growth Program to scale production tenfold and run commercial trials in cosmetics packaging and fashion.

🚪 Market Movements

→ Acquisitions, listings, etc.

Pay.com.au, the Sydney-based B2B fintech that lets businesses earn credit card points on bills and tax payments, paused its planned ASX IPO amid Middle East-driven market volatility and instead closed a A$20 million private placement at a A$750 million valuation, down from the A$850 million it was targeting for a public float.

Protecht, the Australian-founded governance, risk and compliance platform, acquired US AI-powered third-party risk platform VISO TRUST to add agentic vendor risk assessment and continuous monitoring capabilities to its global platform.

💸 New Funds

→ Fresh VC capital announcements

Beaten Zone Venture Partners, Steve Baxter’s Australia-focused defence tech fund, has secured A$17 million in committed capital, targeting autonomous systems, advanced hardware, and cyber resilience as geopolitical instability drives a meaningful shift in VC sentiment toward sovereign capability.

Hiraya Ventures, the family office of Kami cofounders established the CIE Alumni Fund at the University of Auckland with a A$30,000 seed gift to support the Velocity startup program, a nod to the campus program that launched Kami, now used by 70 million people across 180 countries.

#random

Tips (the non-pecuniary kind)

Shipping something cool or has some gossip worth sharing in the startup world? Please send it to us at lucas@ryft.vc or julia@ryft.vc.